Week 16: Revenue Integrity and Cap Rates | The Other 5%

Why Clean Revenue Systems Create Exit Confidence

----------------------------

When owners think about valuation, the conversation usually starts with census.

Occupancy. Rate. NOI. Cap rates.

Those metrics deserve the attention they receive.

But there is another factor quietly influencing every transaction that rarely makes it into the boardroom discussion.

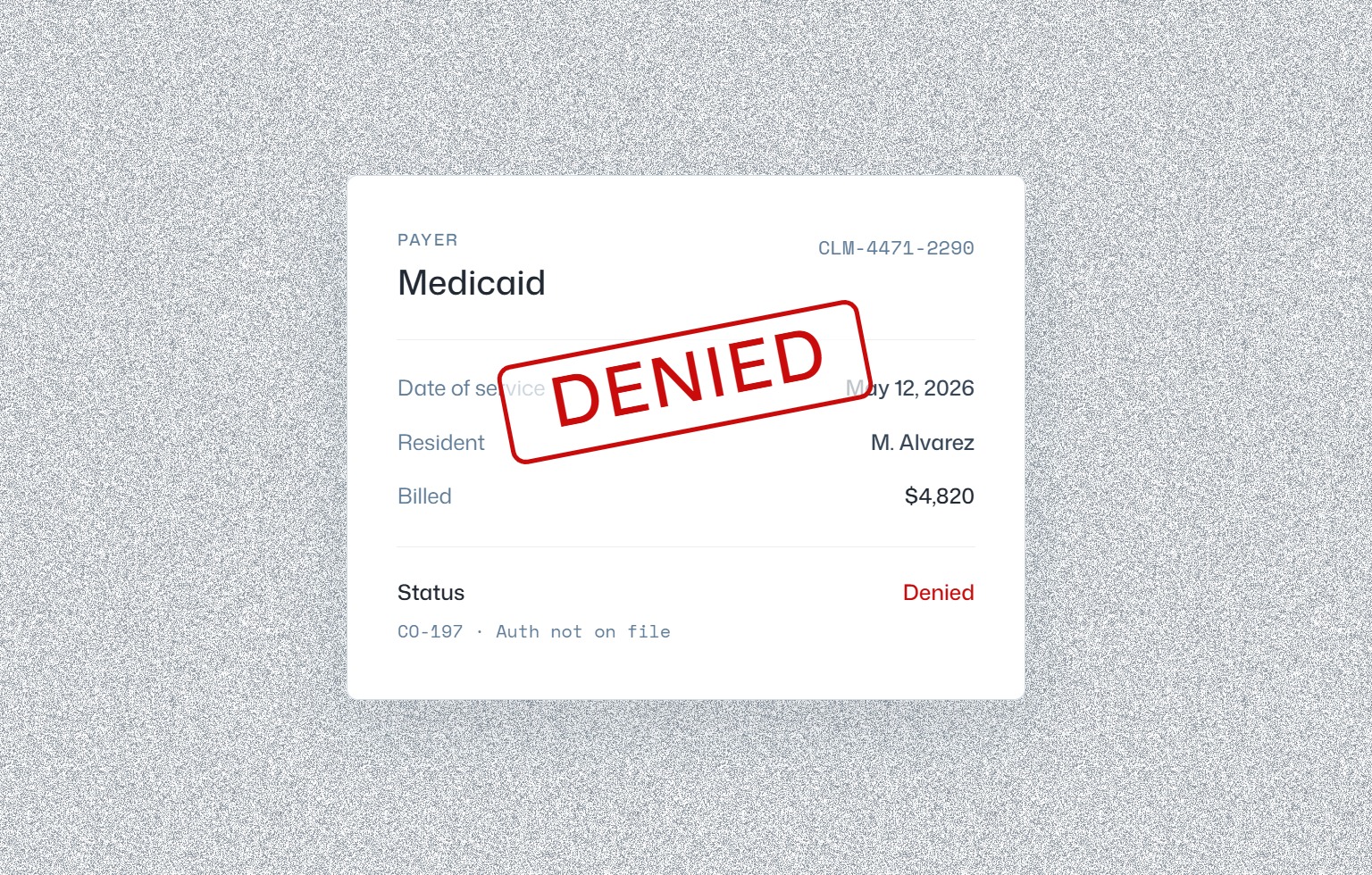

Revenue integrity.

Because booked revenue and collected revenue are not the same thing.

A community can report strong top-line performance while simultaneously struggling with denials, delayed collections, unresolved balances, and aging receivables. On paper, the income statement may look healthy. In reality, cash flow may tell a very different story.

And sophisticated buyers know the difference.

When a lender, investor, or acquisition team begins evaluating an opportunity, they are not simply reviewing financial statements. They are assessing risk.

Their question is not:

"How much revenue does this community generate?"

Their question is:

"How much of that revenue reliably becomes cash?"

That distinction matters.

A million dollars of revenue that consistently reaches the bank account is fundamentally different from a million dollars of revenue that requires constant intervention, produces recurring write-offs, or remains trapped in accounts receivable.

Both may appear identical on an income statement.

They do not feel identical during due diligence.

Every transaction includes a search for surprises.

Unresolved claims. Growing receivable balances. Documentation gaps. Collection challenges. Revenue adjustments.

These issues create uncertainty.

And uncertainty has a cost.

The more questions a buyer must answer during diligence, the more risk they perceive in the investment.

The more risk they perceive, the more pressure there is on valuation.

This is especially important in today's environment.

Valuations across multiple asset classes remain elevated. Competition for quality investments continues to drive pricing. Investors are often willing to pay premium multiples for opportunities that demonstrate predictable performance.

Predictability is valuable. Confidence is valuable. Visibility is valuable.

When a buyer can clearly see that revenue is being captured correctly, billed appropriately, collected efficiently, and reconciled consistently, it changes the conversation.

Instead of debating revenue quality, they can focus on future opportunity.

Instead of building reserves for potential collection issues, they can focus on growth.

Instead of worrying about an unexpected capital call after closing, they can underwrite with greater confidence.

That confidence has real value.

Revenue integrity is often viewed as an operational issue.

It is not.

It is a valuation issue.

Every denied claim that sits unresolved. Every recurring billing error. Every unexplained adjustment. Every balance that ages without resolution.

Those are not simply accounting challenges.

They are signals.

Signals that investors, lenders, and buyers notice.

The opposite is also true.

Clean revenue systems send a signal.

They demonstrate discipline. They demonstrate accountability. They demonstrate operational consistency.

Most importantly, they demonstrate that reported financial performance can be trusted.

And trust is one of the most valuable assets any organization can bring to a transaction.

Long before a community enters a sale process, seeks refinancing, or raises capital, it is building a reputation through its revenue practices.

Every successful collection. Every resolved denial. Every reconciled account. Every month of clean reporting.

Those efforts compound over time.

Not just into stronger cash flow.

Into stronger confidence.

Because at the end of the day, investors are not buying revenue.

They are buying the expectation of future cash flow.

The organizations that can prove the connection between the income statement and the bank account will always have an advantage.

That advantage may never appear on a monthly operating report.

But it often becomes visible when valuation discussions begin.

And that is exactly where The Other 5% lives.

—JT